UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

SCHEDULE 14A

Proxy Statement Pursuant to Section 14(a) of the

Securities Exchange Act of 1934

(Amendment No.___)

Filed by the Registrant x

Filed by a Party other than the Registrant ¨

Check the appropriate box:

¨x Preliminary Proxy Statement

¨ Confidential, for Use of the Commission Only (as permitted by Rule 14a-6(e)(2))

x¨ Definitive Proxy Statement

¨ Definitive Additional Materials

¨ Soliciting Material Pursuant to §240.14a-12

Strategic Realty Trust, Inc.

(Name of Registrant as Specified In Its Charter)

(Name of Person(s) Filing Proxy Statement, if other than the Registrant)

Payment of Filing Fee (Check the appropriate box):

x¨ No fee required.

¨ Fee computed on table below per Exchange Act Rules 14a-6(i)(1) and 0-11.

(1) Title of each class of securities to which transaction applies:

(2) Aggregate number of securities to which transaction applies:

(3) Per unit price or other underlying value of transaction computed pursuant to Exchange Act Rule 0-11 (set forth the amount on which the filing fee is calculated and state how it was determined):

(4) Proposed maximum aggregate value of transaction:

(5) Total fee paid:

¨ Fee paid previously with preliminary materials.

¨x Check box if any part of the fee is offset as providedFee computed on table in exhibit required by Item 25(b) per Exchange Act Rule 0-11(a)(2)Rules 14a-6(i)(1) and identify the filing for which the offsetting fee was paid previously. Identify the previous filing by registration statement number, or the Form or Schedule and the date of its filing.0-11.

(1) Amount Previously Paid:

(2) Form, Schedule or Registration Statement No.:

(3) Filing Party:

(4) Date Filed:

Dear Stockholder:

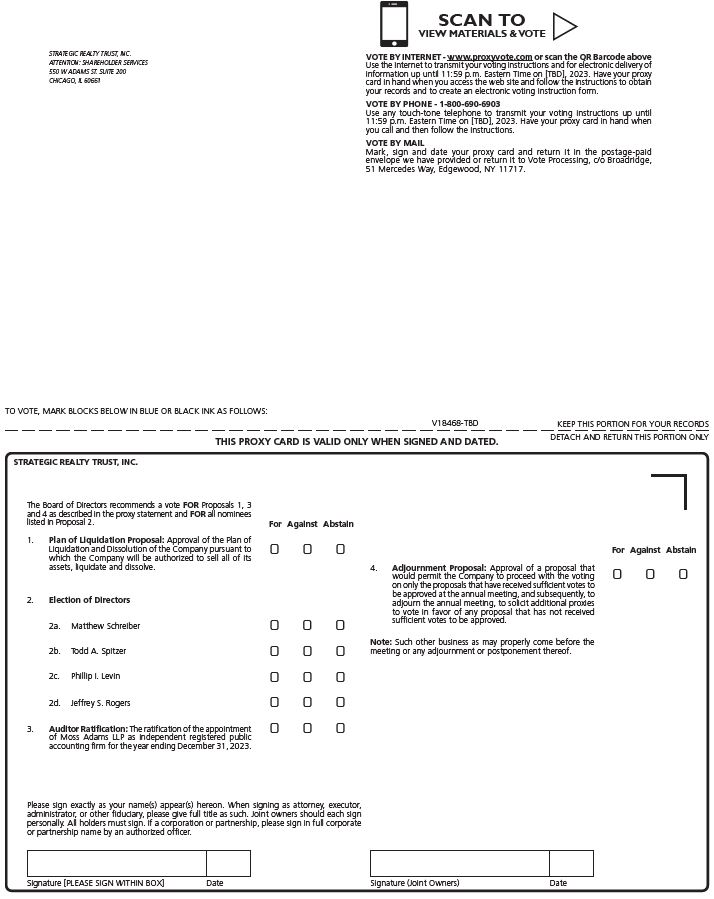

You are cordially invited to attend the annual meeting of the stockholders of Strategic Realty Trust, Inc. (“we,” “us,” or the “Company”) to be held on [•], 2023, at [•]. The meeting will begin at [•] Pacific Time.

At the annual meeting, we will seek your approval of: (i) a plan of complete liquidation and dissolution of the Company (the “Plan of Liquidation,” and the proposal, the “Plan of Liquidation Proposal”), (ii) the election of four directors, (iii) the ratification of the appointment of Moss Adams LLP as our independent registered public accounting firm for the fiscal year ending December 31, 2023, and (iv) a proposal that would permit us to proceed with the voting on and approval of only the proposals that have received sufficient votes to be approved at the annual meeting and, subsequently, to adjourn the annual meeting to solicit additional proxies to vote in favor of any proposal that has not received sufficient votes to be approved at the annual meeting, if necessary (the “Adjournment Proposal”).

The principal purpose of the Plan of Liquidation is to provide liquidity to our stockholders by selling our properties, paying our debts and distributing the net proceeds from liquidation to you.

Our board of directors (the “Board”) has carefully reviewed and considered the alternatives reasonably available to us at this time, as well as the presentation by Robert A. Stanger & Co., Inc. to the Board regarding its opinion as to the reasonableness, from a financial point of view, of our estimated range of liquidating distributions per share to be received by our stockholders in a liquidation pursuant to the Plan of Liquidation, the terms and conditions of the Plan of Liquidation and the types of transactions contemplated by the Plan of Liquidation. The Board unanimously determined that a planned liquidation pursuant to the Plan of Liquidation as more fully described in the attached proxy statement will be more likely to maximize stockholder value at this time and that the terms of the Plan of Liquidation are advisable and in your best interest and unanimously approved the sale of all of our assets and our dissolution pursuant to the Plan of Liquidation, pending your approval. Accordingly, the Board unanimously recommends that you vote FOR approval of the Plan of Liquidation.

In reaching these conclusions, our Board reviewed the other alternatives described in the enclosed proxy statement and considered a number of factors, each of which is discussed in more detail in the enclosed proxy statement, which we believe have made a planned liquidation pursuant to the Plan of Liquidation more likely to maximize stockholder value at this time. We currently estimate that if the Plan of Liquidation Proposal is approved by our stockholders and we are able to implement the plan successfully, our liquidating distributions per share and, therefore, the amount of cash that you would receive for each share of our common stock that you then hold, would range between approximately $1.11 and $1.42 per share.

Your vote is very important. As discussed in the enclosed proxy statement, the Board believes that the Plan of Liquidation is the best alternative reasonably available to us to maximize stockholder returns at this time due to the Company’s declining liquidity and ongoing operating expenses. We cannot complete the sale of all of our properties and our dissolution pursuant to the terms of the Plan of Liquidation without the affirmative vote of a majority of all of the shares of common stock entitled to vote on the matter and the Board encourages you to vote as soon as possible in order that stockholder returns in a liquidity event may be maximized.

The Board also recommends that you vote FOR all of the nominated directors, FOR the ratification of the appointment of Moss Adams LLP as the Company’s independent registered public accounting firm for the fiscal year ending December 31, 2023, and FOR the Adjournment Proposal.

Whether or not you plan to attend the annual meeting, please complete, sign, date and return the enclosed proxy card, or submit your proxy by telephone or the Internet, if eligible, as soon as possible. If you hold your shares in “street name,” you should instruct your broker how to vote in accordance with your voting instruction card.

You are encouraged to review carefully the enclosed proxy statement, as it explains the reasons for the proposals to be voted on at the annual meeting and contains other important information, including a copy of the Plan of Liquidation, which is attached at Annex A. In particular, please review the matters referred to under “Risk Factors” for a discussion of the risks related to the Plan of Liquidation.

| | |

Sincerely,

Matthew Schreiber.Chief Executive Officer |

STRATEGIC REALTY TRUST, INC.

P.O. Box 5049550 W. Adams St., Suite 200

San Mateo, California 94402Chicago, Illinois, 60661

NOTICE OF 20212023 ANNUAL MEETING OF STOCKHOLDERS

AND INTERNET AVAILABILITY OF PROXY MATERIALS

Dear Stockholder:

On Wednesday June 23, 2021, [•], 2023, Strategic Realty Trust, Inc. (“we,” “us,” or the Company”) will hold our 2021the 2023 annual meeting of stockholders at the Crowne Plaza, 1221 Chess Drive, Foster City, California 94404.[•]. The meeting will begin at 9:00 a.m.[•] Pacific Time.

We are holding this meeting to:

1.Approve a plan of complete liquidation and dissolution of the Company, as more fully described in the accompanying proxy statement (the “Plan of Liquidation”). The proposal related to the Plan of Liquidation is referred to herein as the “Plan of Liquidation Proposal.” The principal purpose of the Plan of Liquidation is to provide liquidity to our stockholders by selling our properties, paying our debts and distributing the net proceeds from liquidation to you.

The board of directors recommends a vote FOR the Plan of Liquidation Proposal.

2.Elect two nominees to the board of directors to serve until the 20222024 annual meeting of stockholders and until their successor(s) are duly elected and qualified, one nominee to the board of directors to serve until the 20232025 annual meeting of stockholders and until his successor is duly elected and qualified, and elect one nominee to the board of directors to serve until 2024the 2026 annual meeting of stockholders and until his successor is duly elected and qualified.

The board of directors recommends a vote FOR these nominees to the board of directors.

2.3.AttendRatify the appointment of Moss Adams LLP as our independent registered public accounting firm for the fiscal year ending December 31, 2023.

The board of directors recommends a vote FOR the ratification of the appointment of Moss Adams LLP as our independent registered public accounting firm for the year ending December 31, 2023.

4.Vote on a proposal that would permit us to such other business as may properly come beforeproceed with the voting on and approval of only the proposals that have received sufficient votes to be approved at the annual meeting, and subsequently, to adjourn the annual meeting, to solicit additional proxies to vote in favor of any adjournments or postponements thereof.proposal that has not received sufficient votes to be approved at the annual meeting (the “Adjournment Proposal”).

The board of directors recommends a vote FOR the Adjournment Proposal.

The board of directors has selected March 22, 2021[•], 2023, as the record date for determining stockholders entitled to vote at the meeting.

This proxy statement and proxy card are being mailed to you on or about April 2, 2021,[•], 2023, along with a copy of our 20202022 annual report.

Whether or not you plan to attend the meeting and vote in person, or not, we urge you to have your vote recorded as early as possible. Please complete, sign and date the accompanying proxy card and return it in the accompanying self-addressed postage-paid return envelope. Alternatively, you may be able to vote over the Internet or by telephone, depending on how your account is registered. Please refer to the instructions on your proxy card.

Your vote is very important! Your immediate response will help avoid potential delays and may save us significant additional expenses associated with soliciting stockholder votes.

IMPORTANT NOTICE REGARDING AVAILABILITY OF PROXY MATERIALS FOR THE ANNUAL MEETING OF STOCKHOLDERS TO BE HELD ON JUNE 23, 2021:[•], 2023:

Our proxy statement, form of proxy card and 20202022 annual report to stockholders are also available at www.srtreit.com.

By Order of the Board of Directors,

Andrew Batinovich

Matthew Schreiber

Chief Executive Officer and Assistant Secretary

April 2, 2021[•], 2023

San Mateo, CaliforniaChicago, Illinois

TABLE OF CONTENTS

STRATEGIC REALTY TRUST, INC.

P.O. Box 5049550 W. Adams St., Suite 200

San Mateo, California 94402Chicago, Illinois, 60661

(650) 343-9300(312) 878-4848

PROXY STATEMENT

Annual Meeting Information and Purpose of Proxy Statement

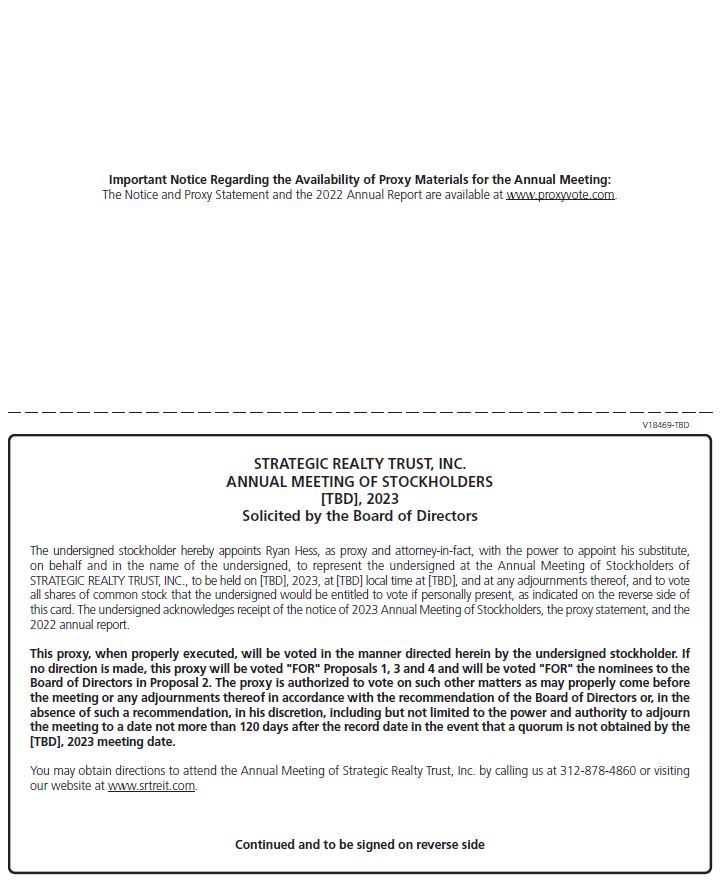

We are providing these proxy materials in connection with the solicitation by the board of directors of Strategic Realty Trust, Inc. (“Strategic Realty Trust,” the “Company,” “we,” “our”“our,” or “us”), a Maryland corporation, of proxies for use at the 20212023 annual meeting of stockholders to be held on June 23, 2021,[•], 2023, at 9:00 a.m.[•] Pacific Time at the Crowne Plaza, 1221 Chess Drive, Foster City, California 94404,[•], and at any adjournments or postponements thereof for the purposes set forth in the accompanying Notice of 20212023 Annual Meeting of Stockholders (the “Notice of 20212023 Annual Meeting”).

This proxy statement, which includes the Notice of 20212023 Annual Meeting, and the accompanying form of proxy and voting instructions are first being mailed or given to stockholders on or about April 2, 2021.[•], 2023.

Annual Report

On or about April 2, 2021,[•], 2023, our Annual Report for the year ended December 31, 20202022 (which includes a copy of our Annual Report on Form 10-K for the year ended December 31, 2020,2022, as filed with the Securities and Exchange Commission (the “SEC”)) was mailed to each of our stockholders of record as of the close of business on March 22, 2021.[•], 2023.

Our Annual Report on Form 10-K, as filed with the SEC, may be accessed online through our website at www.srtreit.com or through the SEC’s website at www.sec.gov. In addition, you may request a copy of our Annual Report on Form 10-K by writing to us at the following address: P.O. Box 5049, San Mateo, California 94402, Attention: Secretary.550 W. Adams St., Suite 200, Chicago, Illinois 60661.

QUESTIONS AND ANSWERS ABOUT THE MEETING, VOTING AND VOTINGTHE PLAN OF LIQUIDATION

The following are some questions that you, as a stockholder of Strategic Realty Trust, Inc. may have regarding the annual meeting, voting and the Plan of Liquidation (defined below) and brief answers to those questions. We urge you to read carefully the remainder of this proxy statement because the information in this section may not provide all the information that might be important to you with respect to the proposals being considered at the annual meeting. Additional important information is also contained in the annexes to, and the documents incorporated by reference in, this proxy statement. In this section and elsewhere in this proxy statement, references to “you” refers to the Company’s stockholders to whom the notice of annual meeting and this proxy statement are addressed.

Questions About the Annual Meeting and Voting.

Q: Why did you send me this proxy statement?

A: We sent you this proxy statement and the enclosed proxy card because our board of directors is soliciting your proxy to vote your shares at the 20212023 annual stockholders meeting. You owned shares of record of our common stock at the close of business on [•], 2023, the record date for the annual meeting, and, therefore, are entitled to vote at the annual meeting. This proxy statement includes information that we are required to provide to you under the rules of the SEC and is designed to assist you in voting. You do not need to attend the annual meeting in person in order to vote.

Q: What is a proxy?

A: A proxy is a person who votes the shares of stock of another person who could not attend a meeting. The term “proxy” also refers to the proxy card or other method of appointing a proxy. When you submit your proxy, you are appointing Julia KholodenkoRyan Hess, Chief Financial Officer of the Company, as your proxy, and you are giving herhim permission to vote your shares of common stock at the annual meeting. The appointed proxy will vote your shares of common stock as you instruct, unless you submit your proxy without instructions. In

If you submit your proxy without instruction, he will vote:

•FOR the proposed plan of complete liquidation and dissolution of the Company, as more fully described in this case, she will vote proxy statement (the “Plan of Liquidation,” and the proposal the “Plan of Liquidation Proposal”),

•FOR the election of the nominees to the board of directors. directors,

•FOR the ratification of the appointment of Moss Adams LLP (“Moss Adams”) as our independent registered public accounting firm for the year ending December 31, 2023, and

•FOR a proposal that would permit us (a) to proceed with the voting on and approval of only the proposals that have received sufficient votes to be approved at the annual meeting, and (b) subsequently, to adjourn the annual meeting to solicit additional proxies to vote in favor of any proposal that has not received sufficient votes to be approved at the annual meeting (the “Adjournment Proposal”).

With respect to any other proposals to be voted upon, shehe will vote in accordance with the recommendation of the board of directors or, in the absence of such a recommendation, in herhis discretion. If you do not submit your proxy, your shares will not be voted at the annual meeting. This is why it is important for you to return your proxy card to us (or authorize a proxy over the Internet or by telephone)telephone, if eligible) as soon as possible whether or not you plan on attending the annual meeting.

Q: When is the annual meeting and where will it be held?

A: The 20212023 annual meeting of stockholders will be held on June 23, 2021,[•], 2023, at 9:00 a.m.[•] Pacific Time at the Crowne Plaza, 1221 Chess Drive, Foster City, California 94404.[•].

Q: What is the purpose of the 20212023 annual meeting?

A: At the 20212023 annual meeting, stockholders will vote on the Plan of Liquidation, the election of four nominees to serve on the board of directors, the ratification of the appointment of Moss Adams as our independent registered public accounting firm for the year ending December 31, 2023, and on any other proposal to be voted on.the Adjournment Proposal.

Management will also report on the status of our portfolio of properties. In addition, representatives of Moss Adams, LLP, our independent registered public accounting firm, (“Moss Adams”), are expected to attend the 20212023 annual meeting, will have an opportunity to make a statement if they so desire, and will be available to respond to questions from our stockholders.

Q: What is the board of directors’ voting recommendation?

A: The board of directors recommends a vote FOR the Plan of Liquidation Proposal,FOR the election of the nominees to the board of directors.directors, FOR the ratification of the appointment of Moss Adams as our independent registered public accounting firm for the year ending December 31, 2023 and FOR the Adjournment Proposal.

Q: Who is entitled to vote?

A: Only stockholders of record at the close of business on March 22, 2021,[•], 2023, the record date, are entitled to receive notice of the annual meeting and to vote the shares of common stock of the Company that they hold on the record date at the annual meeting, or any postponements or adjournments thereof. As of the record date, there were 10,739,814[•] shares of common stock issued and outstanding and entitled to vote. Each outstanding share of common stock entitles its holder to cast one vote on each proposal to be voted on.

Q: What constitutes a quorum?

A: A quorum consists of the presence in person or by proxy of stockholders entitled to cast 50% of all the votes entitled to be cast at the annual meeting. There must be a quorum present in order for the annual meeting to be a duly held meeting at which business can be conducted. Generally, if you submit your proxy, even if you abstain from voting, then you will at leaststill be considered part of the quorum. Abstentions and broker non-votes will be counted to determine whether

If a quorum is present. A broker “non-vote” occurs when a broker, banknot present at the annual meeting, the chairman of the meeting may adjourn the annual meeting to another date, time or other nominee holding shares for a beneficial ownerplace, not later than 120 days after the original record date of [•], 2023. Notice need not be given of the new date, time or place if announced at the annual meeting before an adjournment is present in person or by proxy but does not vote on a particular proposal because the nominee does not have discretionary voting power with respect to that matter and has not received voting instructions from the beneficial owner.taken.

Q: Can I attend the annual meeting?

A: You are invited to attend the annual meeting if you were a stockholder of record or a beneficial holder as of the close of business on March 22, 2021,[•], 2023, or you hold a valid legal proxy for the 20212023 annual meeting. If you are the stockholder of record, your name will be verified against the list of stockholders of record prior to your being admitted to the annual meeting. You should be prepared to present photo identification for admission. If you are a beneficial holder, you will need to provide proof of beneficial ownership on the record date as well as your photo identification, for admission. If you do not provide photo identification or comply with the other procedures outlined above upon request, you may not be admitted to the annual meeting.

Q: How do I vote my shares?

A: Stockholders of record may vote their shares in the following manner:

•Authorizing a Proxy by Mail — Stockholders may authorize a proxy by completing the accompanying proxy card and mailing it in the accompanying self-addressed postage-paid return envelope.

•Authorizing a Proxy via the Internet — Eligible stockholders may authorize a proxy by going to www.proxyvote.com and following the online instructions.

•Authorizing a Proxy by Telephone — Eligible stockholders may authorize a proxy by calling 1-800-690-6903 and following the recorded instructions.

•In Person at the Meeting — Stockholders of record may vote in person at the annual meeting. Written ballots will be passed out to those stockholders who want to vote at the meeting.

For those stockholders eligible to vote by Internet, we encourage you to do so, since this method of voting is quick, convenient, and cost-efficient. Please refer to your proxy card to see if you are eligible to vote by telephone or Internet.internet. When you vote via the Internet or by telephone prior to the annual meeting date, your vote is recorded immediately and there is no risk that postal delays will cause your vote to arrive late and, therefore, not be counted.

If your shares are held by a bank, broker or other nominee (that is, in “street name”), you are considered the beneficial owner of your shares and you should refer to the instructions provided by your bank, broker or nominee regarding how to vote. In addition, because a beneficial owner is not the stockholder of record, you may not vote shares held by a bank, broker or nominee in street name at the annual meeting unless you obtain a “legal proxy” from the bank, broker or nominee that holds your shares, giving you the right to vote the shares at the meeting.

If you elect to attend the meeting, you can submit your vote in person, and any previous votes that you submitted will be superseded. If you return your signed proxy, your shares will be voted as you instruct, unless you give no instructions with respect to one or more of the proposals.In this case, unless you later instruct otherwise, your shares of common stock will be voted FOR the nominees to the board of directors. With respect to any other proposals to be voted on, your shares of common stock will be voted in accordance with the recommendation of the board of directors or, in the absence of such a recommendation, in the discretion of Ms. Kholodenko.

Q: What if I submit my proxy and then change my mind?

A: You have the right to revoke your proxy at any time before the annual meeting by:

•delivering to our secretary a written notice of revocation;

•returning a properly signed proxy bearing a later date; or

•attending the annual meeting and voting in person (although attendance at the annual meeting will not cause your previously granted proxy to be revoked unless you specifically so request).

To revoke a proxy previously submitted by mail or authorized via telephone or the Internet, you may simply authorize a proxy again at a later date using one of the procedures set forth above, but before the deadline for mail, telephone, or Internet voting, in which case the later submitted proxy will be recorded and the earlier proxy revoked.

If you hold shares of our common stock in “street name,” you will need to contact the institution thata broker or other nominee holds your shares and follow its instructions for revoking a proxy.stock on your behalf, you must contact your broker, bank or other nominee to change your vote.

Q: What happens if additional proposals are presented at the annual meeting?

A: Other than the matters described in this proxy statement, we do not expect any additional matters to be presented for a vote at the annual meeting. If other matters are presented and you are voting by proxy, your proxy grants the individuals named as proxy holders the discretion to vote your shares on any additional matters properly presented for a vote at the meeting.

Q: Will my vote make a difference?

A: Yes. Your vote could affect the composition of our board of directors.proposals described in this proxy statement. Moreover, your vote is needed to ensure that a quorum is present at the annual meeting so that the proposals can be acted upon. YOUR VOTE IS VERY IMPORTANT! Your immediate response will help avoid potential delays and may save us significant additional expenses associated with soliciting stockholder votes.

Q. What are the voting requirements for the Plan of Liquidation Proposal?

A: The affirmative vote of a majority of all of the shares of common stock entitled to vote on the Plan of Liquidation Proposal is required for approval of the Plan of Liquidation Proposal. Because of this majority vote requirement, “ABSTAIN” votes and broker non-votes (discussed below) will have the effect of a vote against the Plan of Liquidation Proposal. If you submit a proxy card with no further instructions, your shares will be voted FOR the Plan of Liquidation Proposal.

Q: What are the voting requirements to elect the director nominees?

A: Under our charter, the election of a director requires the affirmative vote of holders of a majority of the shares entitled to vote who are present in person or by proxy at an annual meeting at which a quorum is present. This means that, of the shares present in person or by proxy at an annual meeting, a director nominee needs to receive affirmative votes from a majority of such shares in order to be elected to the board of directors. Because of this majority vote requirement, “withhold” votesabstentions and broker non-votes will have the effect of a vote against each nominee for director. If an incumbent director nominee fails to receive the required number of votes for reelection, then under Maryland law, he or she will continue to serve as a “holdover”

“holdover” director until his or her successor is duly elected and qualified. If you submit a proxy card with no further instructions, your shares will be voted in accordance withFOR each nominee.

Q: What are the recommendationvoting requirements for the ratification of the boardappointment of directors.Moss Adams as our independent registered public accounting firm for the year ending December 31, 2023?

A: A majority of the votes cast at an annual meeting at which a quorum is present is required for the ratification of the appointment of Moss Adams as our independent registered public accounting firm for the year ending December 31, 2023. Abstentions will have no effect on the determination of this proposal. Your shares may be voted for this proposal if they are held in the name of a brokerage firm even if you do not provide the brokerage firm with voting instructions. If you submit a proxy card with no further instructions, your shares will be voted FOR the ratification of the appointment of Moss Adams as our independent registered public accounting firm for the year ending December 31, 2023.

Q: What are the voting requirements to approve the Adjournment Proposal?

A: A majority of the votes cast at an annual meeting at which a quorum is present is required for the approval of the Adjournment Proposal. Abstentions and broker non-votes will not affect the outcome of this proposal. If you submit a proxy card with no further instructions, your shares will be voted FOR the Adjournment Proposal.

Q: What is a “broker non-vote”?

A: A “broker non-vote” occurs when a broker holding stock on behalf of a beneficial owner submits a proxy but does not vote on a particular proposal because the broker does not have discretionary voting power with respect to that particular proposal and has not received instructions from the beneficial owner. Brokers are precluded from exercising their voting discretion with respect to the approval of non-routine matters, such as the approval of the Plan of Liquidation Proposal and, as a result, absent specific instructions from the beneficial owner of such shares, brokers will not vote those shares. Broker non-votes will be considered as “present” for purposes of determining a quorum. Broker non-votes will have the effect of a vote AGAINST the Plan of Liquidation Proposal and AGAINST each nominee for director and no effect on the Adjournment Proposal. Because brokers have discretionary authority to vote for the ratification of the appointment of Moss Adams LLP as our independent registered public accounting firm, in the event they do not receive voting instructions from the beneficial owner of the shares, there will not be any broker non-votes with respect to that proposal.

Your broker will send you information to instruct it on how to vote on your behalf. If you do not receive a voting instruction card from your broker, please contact your broker promptly to obtain a voting instruction card. Your vote is important to the success of the proposals. We encourage all of our stockholders whose shares are held by a broker to provide their brokers with instructions on how to vote.

Q: How are proxies being solicited?

A: In addition to mailing proxy solicitation materials, our directors and employees of our advisor or its affiliates may also solicit proxies in person, via the Internet, by telephone or by any other electronic means of communication we deem appropriate. Additionally, we have retained Broadridge Financial Solutions, Inc. (“Broadridge”), a proxy solicitation firm, to assist us in the proxy solicitation process. If you need any assistance, or have any questions regarding the proposals or how to cast your vote, you may contact Broadridge at (888) 777-1346.

Q: Who will bear the costs of soliciting votes for the meeting?

A: The Company will bear the entire cost of its solicitation of proxies from its stockholders. In addition to the mailing of these proxy materials, the solicitation of proxies or votes may be made in person, by telephone or by electronic communication by ourOur directors, officers and employees of our advisor and its affiliates who will not receive any additional compensation for such solicitation activities. We anticipate that for Broadridge’s solicitation services we will pay approximately $40,000, plus reimbursement of Broadridge’s out-of-pocket expenses. We will also reimburse brokerage houses and other custodians, nominees and fiduciaries for their reasonable out-of-pocket expenses for forwarding proxy solicitation materials to our stockholders.

Q: Who will count the votes?

A: The board of directors will appoint an independent inspector of elections to tabulate the votes.

Q. What should I do if I receive more than one set of voting materials for the annual meeting?

A. You may receive more than one set of voting materials for the annual meeting, including multiple copies of this proxy statement and multiple proxy cards or voting instruction forms. For example, if you hold your shares in more than one brokerage account, you will receive a separate voting instruction form for each brokerage account in which you hold shares. If you are a holder of record and your shares are registered in more than one name, you will receive more than one proxy card and voting instruction form. For each and every proxy card and voting instruction form that you receive, please authorize a proxy as soon as possible using one of the following methods:

•Authorizing a Proxy by Mail — Stockholders may authorize a proxy by completing the accompanying proxy card and mailing it in the accompanying self-addressed postage-paid return envelope.

•Authorizing a Proxy via the Internet — Eligible stockholders may authorize a proxy by going to www.proxyvote.com and following the online instructions.

•Authorizing a Proxy by Telephone — Eligible stockholders may authorize a proxy by calling 1-800-690-6903 and following the recorded instructions.

•In Person at the Meeting — Stockholders of record may vote in person at the annual meeting. Written ballots will be passed out to those stockholders who want to vote at the meeting.

Q. What should I do if only one set of voting materials for the annual meeting is sent and there are multiple Company stockholders in my household?

A. Some banks, brokers and other nominee record holders may be participating in the practice of “householding” proxy statements and annual reports. This means that only one copy of this proxy statement may have been sent to multiple stockholders in your household. We will promptly deliver a separate copy of this proxy statement to you if you contact Broadridge at 800-574-5897.

Q: Where can I find the voting results of the annual meeting?

A: The Company will report voting results in a Current Report on Form 8-K filed with the SEC within four business days following the annual meeting. If final voting results are not known when such report is filed, they will be announced in an amendment to such report within four business days after the final results become known.

Q: Where can I find more information?

A: We file annual, quarterly, current reports and otherAdditional information with the SEC. Copies of SEC filings, including exhibits,about us can be obtained freefrom the various sources described under “Where You Can Find More Information” in this proxy statement.

Questions About the Plan of chargeLiquidation Proposal

Q. Why is the Plan of Liquidation Proposal being made?

A. We were formed in September 2008 as a Maryland corporation and have elected annually to be taxed as a real estate investment trust (“REIT”) beginning with the taxable year ended December 31, 2009.

From August 7, 2009 through February 7, 2013, we conducted an initial public offering pursuant to which we raised $104.7 million in gross primary offering proceeds through the sale of 10,688,940 shares of common stock and an additional $3.6 million in gross offering proceeds through the sale of 391,182 shares of common stock in our distribution reinvestment plan.

With the net proceeds from the initial public offering, we pursued a strategy of investing in income-producing retail properties and specifically, acquiring high-quality urban retail properties in major west coast markets. Following our transition to a new advisor in August 2013, our board of directors pursued a strategic plan to recycle equity from properties held at the time of the transition, which we refer to as “legacy properties,” with the goal that a fully recycled and focused high-quality west coast urban retail portfolio would maximize stockholder returns over the long term. In April 2021, we completed the sale of our last legacy property, Shops at Turkey Creek (the property was initially under contract in January 2020; however, the original buyer canceled the contract due to the uncertainty of the COVID-19 pandemic on the real estate lending and financial markets). Following the sale, an undeveloped land parcel remains the only legacy property in the portfolio.

In 2020 our websitefocus necessarily shifted from completing the strategic recycling of the portfolio to guiding the portfolio through the COVID-19 pandemic and then expediting the portfolio’s recovery from the COVID-19 pandemic and other macroeconomic headwinds. In the fourth quarter of 2022, in furtherance of this goal, we completed the sale of 3032 Wilshire and Sunset & Gardner, two development projects that accounted for a majority of our GAAP net losses during the previous three years. Following the sale of the two develop projects, our current portfolio consists of six retail properties, excluding an undeveloped land parcel, comprising an aggregate of approximately 27,000 square feet of multi-tenant, retail space located in California.

As part of its ongoing oversight, direction and management of the Company, our board of directors and management team regularly review and discuss the Company’s performance, business plan, strategic direction and future prospects. In particular, our board of directors has been focused on positioning the Company for a liquidity event for some time given the Company’s status as a non-traded REIT and the fact that many of our investors have held their shares for between 10 and 14 years and the share redemption program has been unavailable to many stockholders for over 10 years.

On February 1, 2023, at www.srtreit.com. This website address is provideda regularly scheduled board meeting following the successful stabilization of the portfolio, the board of directors requested that SRT Advisor, LLC (“SRT Advisor”), our external advisor, work with DLA Piper LLP (US) (“DLA Piper”), outside legal counsel to the Company, to prepare a presentation for your informationthe board of directors regarding a liquidation strategy for the Company.

On March 1, 2023, the board of directors held a meeting at which a representative of DLA Piper reviewed with the board of directors an outline of the process and convenience. Our website is not incorporated intoconsiderations for the liquidation and dissolution of the Company.

On April 5, 2023, the board of directors held a meeting at which SRT Advisor reviewed the strategic alternatives available to the Company and recommended moving forward with a plan of liquidation. SRT Advisor presented a number of considerations, including (i) the limited number of the Company’s assets, (ii) the Company’s performance since inception, (iii) the declining prospects for the Company’s financial viability and future ability to meet its expenses as a public reporting company and (iv) alternatives to liquidation, including continuing under the current business plan, raising additional capital, and seeking to dispose of our assets through a merger or a portfolio sale. After reviewing the alternatives reasonably available to us, the board of directors determined, based on the recommendation of SRT Advisor, that it was in our best interest and the best interest of our stockholders to proceed with pursuing a liquidation strategy through asset sales and authorized SRT Advisor to develop a plan of liquidation for approval by our board of directors and submission to our stockholders.

On April 10, 2023, the Company retained Robert A. Stanger & Co., Inc. (“Stanger”) to deliver an opinion regarding the reasonableness, from a financial point of view, of our estimated range of liquidating distributions per share as prepared by management, should the board of directors determine to approve a plan of liquidation and dissolution

On May 12, 2023, the board of directors held a meeting to review the liquidation strategy prepared by SRT Advisor. Also in attendance at the meeting were members of management as well as a representative from the Company’s outside legal counsel and Stanger, reasonableness opinion provider to the board of directors. At that meeting, SRT Advisor recommended to the board of directors that it would be in our best interest and the best interest of our stockholders to engage in a planned liquidation pursuant to the Plan of Liquidation.

The board of directors carefully reviewed and considered the terms and conditions of the Plan of Liquidation and the transactions contemplated by that plan, as well as the other alternatives described in this proxy statement, and should notthe board of directors reviewed the opinion and presentation by Stanger as to the reasonableness, from a financial point of view, of management’s estimated range of liquidating distributions per share to be considered partreceived by our stockholders in a planned liquidation pursuant to the Plan of Liquidation. See “What alternatives to the Plan of Liquidation have you considered?” below for a discussion of other alternatives considered.

Following a thorough discussion, on May 12, 2023, the board of directors concluded that a planned liquidation pursuant to the Plan of Liquidation was in the Company’s best interest and the best interest of our stockholders and unanimously determined that the terms of the Plan of Liquidation are advisable and in your best interest. For a discussion of the reasons for the Plan of Liquidation, see “Proposal 1. The Plan of Liquidation Proposal – Reasons for the Plan of Liquidation Proposal; Recommendation of the Board of Directors.” The board of directors also unanimously recommended that our stockholders approve the Plan of Liquidation Proposal. Based on the most recent information available to us, we currently estimate that if the Plan of Liquidation Proposal is approved by our stockholders and we are able to implement the plan successfully, our liquidating distributions per share and, therefore, the amount of cash that you would receive for each share of our common stock that you then hold, would range between approximately $1.11 and $1.42 per share.

Our range of estimated liquidating distributions per share is based upon market, economic, financial and other circumstances and conditions existing as of the date of this proxy statement. Additionally,The ongoing challenges affecting the U.S. commercial real estate industry is one of the most significant risks and uncertainties we face with respect to the Plan of Liquidation and the ultimate amount of liquidating distributions received by stockholders. The combination of the continued economic slowdown, rising interest rates and significant inflation (or the perception that any of these events may continue) as well as a lack of lending activity in the debt markets have contributed to considerable weakness in the commercial real estate markets. Moreover, valuations for U.S. commercial retail properties continue to fluctuate due to weakness in the current real estate capital markets as a result of the factors above and the lack of transaction volume for U.S. commercial retail properties, increasing the uncertainty of valuations in the current market environment. All of these factors could adversely impact the amount of liquidating distributions we pay to our stockholders.

Q. What will happen if the Plan of Liquidation Proposal is not approved by our stockholders?

A: We cannot complete the sale of all of our assets or our dissolution pursuant to the terms of the Plan of Liquidation unless our stockholders approve the Plan of Liquidation Proposal. If the Plan of Liquidation Proposal is not approved by our stockholders, the board of directors will meet to determine what other alternatives to pursue in the best interest of the Company and our stockholders, including, without limitation, continuing to operate under our current business plan or seeking approval of a plan of liquidation at a future date.

Q. What alternatives to the Plan of Liquidation have you may readconsidered?

A. Our board of directors also explored the options of:

•continuing under the current business plan;

•raising additional capital; and copy any reports, statements or other information we file with the SEC on the website maintained by the SEC at http://www.sec.gov.

•seeking to dispose of our assets through a merger or a portfolio sale.

After reviewing the other alternatives, and taking into account the currently limited cash available to the Company, the significant expenses associated with operating as a public REIT, our limited portfolio of investments, as well as the current status of our operations and declining liquidity, the board of directors concluded that a planned liquidation pursuant to the Plan of Liquidation was in the Company’s best interest and the best interest of our stockholders. For additional information on the board of directors’ analysis of other strategic alternatives, see “Proposal 1. The Plan of Liquidation Proposal – Background of the Plan of Liquidation – Assessment of Strategic Alternatives.”

Q. What factors have most significantly impacted the net asset value of the Company and resulting range in net proceeds from liquidation?

A. With a limited real estate portfolio of urban retail properties concentrated in California, and San Francisco in particular, downturns in California geographic markets have had a more significant adverse impact on the net asset value of the Company than if the Company had been able to invest in a more diversified investment portfolio. In particular, California instituted some of the most stringent mitigation policies in response to the COVID-19 pandemic and the majority of the Company’s tenants were required to close their stores at one point during the pandemic and/or operate with significant restrictions. In addition, the Company’s operations have been impacted by the particularly tenant-friendly government mandates adopted by the City of San Francisco that limited landlords’ ability to evict tenants and collect rent. Also, the Company had invested in two development projects, 3032 Wilshire and Sunset & Gardner, which suffered from derailed leasing momentum as a result of the pandemic, and accounted for a majority of the Company’s net losses during the previous three years.

Q. Do I have appraisal or dissenters rights in connection with the liquidation?

A. Pursuant to Maryland law and the charter, you are not entitled to appraisal or dissenters rights (or rights of an objecting stockholder) in connection with the Plan of Liquidation.

Q. What is the Plan of Liquidation?

A. The Plan of Liquidation authorizes us to undertake an orderly liquidation. In an orderly liquidation, we would sell all of our assets, pay all of our known liabilities, provide for the payment of our unknown or contingent liabilities, distribute our remaining cash to our stockholders, wind up our operations and dissolve.

In order to dissolve, we will file articles of dissolution (“Articles of Dissolution”) with the State Department of Assessments and Taxation of Maryland (the “SDAT”), our jurisdiction of incorporation, to dissolve the Company as a legal entity following the satisfaction of or provision for all our outstanding liabilities. The board of directors, in its sole discretion, will determine the timing for this filing. We may pay multiple, or a single, liquidating distribution(s) to our stockholders during the liquidation process. We will pay the final liquidating distribution after we sell all of our assets, pay or provide for all of our known liabilities and provide for unknown liabilities. We expect to complete these activities within 24 months after stockholder approval of the Plan of Liquidation. However, the completion of these activities may be delayed due to the ongoing challenges affecting the U.S. commercial real estate industry, including the continued economic slowdown, rising interest rates and significant inflation (or the perception that any of these events may continue), and a lack of lending activity in the debt markets which may impact the ability of buyers for our properties to obtain favorable financing. A final liquidating distribution to our stockholders may not be paid until all of our liabilities have been satisfied. Upon our liquidation and dissolution, the Company will cease to exist.

Q. What are the key provisions of the Plan of Liquidation?

A. The Plan of Liquidation provides, in pertinent part, that, among other things:

•We will be authorized to sell all of our assets, liquidate and dissolve the Company, and distribute the net proceeds from liquidation in accordance with the provisions of the charter and applicable law. Although we currently anticipate that we will sell our assets for cash and our discussion in this proxy statement contemplates that we will receive cash for the sale of our assets, the Plan of Liquidation provides that our assets may be sold for cash, notes or such other assets as may be conveniently liquidated or distributed to our stockholders.

•We will be authorized to take all necessary or advisable actions to wind up our business, pay our debts, and distribute the remaining proceeds to our stockholders.

•We will be authorized to provide for the payment of any unascertained or contingent liabilities. We may do so by purchasing insurance, by establishing a reserve fund or in other ways.

•We expect to distribute all of the net proceeds from liquidation to you within 24 months after the date the Plan of Liquidation is approved by our stockholders. However, the sale of assets and distribution of the net proceeds may be delayed due to the rising interest rate environment that is impacting the ability of buyers to obtain favorable financing, along with the elevated market and economic volatility and persistent concerns over inflation and the continuing impact of the COVID-19 pandemic on U.S. business and economic conditions. If we cannot sell our assets and pay our debts within 24 months, or if the board of directors determines that it is otherwise advisable to do so, we may transfer and assign our remaining assets to a liquidating trust. Upon such transfer and assignment, our stockholders will receive beneficial interests in the liquidating trust. The liquidating trust will pay or provide for all of our liabilities and distribute any remaining net proceeds from liquidation to the holders of beneficial interests in the liquidating trust. The amounts that you would receive from the liquidating trust are included in our estimates described above of the total amount of cash that you will receive in the liquidation.

•Prior to the acceptance for record of the Articles of Dissolution by the SDAT, the board of directors may terminate the Plan of Liquidation for any reason, subject to and contingent upon the approval of such termination by our stockholders. Notwithstanding approval of the Plan of Liquidation by our stockholders, the board of directors or, if a liquidating trust is established, the trustees of the liquidating trust, may make certain modifications or amendments to the Plan of Liquidation without further action by or approval of our stockholders to the extent permitted under law.

•Upon our liquidation and dissolution, all of our outstanding shares of stock will be cancelled and the Company will cease to exist.

For more information, see “Proposal 1: The Plan of Liquidation Proposal.”

Q. Do you have agreements to sell your assets?

A. As of the date of this proxy statement, we have not entered into any agreements to sell our remaining assets.

Q: Did you obtain an opinion about the estimated range of aggregate liquidating distributions?

A: Yes. Stanger provided an opinion, dated May 12, 2023, to the board of directors, as to the reasonableness, from a financial point of view, of management’s estimated range of liquidating distributions per share to be received by our stockholders in a planned liquidation pursuant to the Plan of Liquidation. The full text of Stanger’s written opinion is attached as Annex B to this proxy statement and is incorporated by reference into this proxy statement. The written opinion sets forth, among other things, the assumptions made, procedures followed, factors considered and limitations on the review undertaken by Stanger in rendering its opinion. Stanger provided its opinion for the information and assistance of the board of directors in connection with its consideration of the Plan of Liquidation. You are encouraged to read the Stanger opinion in its entirety. The Stanger opinion constitutes neither a recommendation to you as to how you should vote on the proposals set forth in this proxy statement nor a guarantee as to the actual amount of consideration that will be received by you under the Plan of Liquidation.

Q. If the Plan of Liquidation Proposal is approved, what do you estimate that the Company’s stockholders will receive?

A. The amount of cash that may ultimately be received by our stockholders is not yet known. However, we currently estimate that if the Plan of Liquidation Proposal is approved by our stockholders and we are able to implement the plan successfully, our liquidating distributions per share and, therefore, the amount of cash that you would receive for each share of our common stock that you then hold, would range between approximately $1.11 and $1.42 per share.

Our range of estimated liquidating distributions per share is based upon market, economic, financial and other circumstances and conditions existing as of the date of this proxy statement. The ongoing challenges affecting the U.S. commercial real estate industry is one of the most significant risks and uncertainties we face with respect to the Plan of Liquidation and the ultimate amount of liquidating distributions received by stockholders. The combination of the continued economic slowdown, rising interest rates and significant inflation (or the perception that any of these events may continue) as well as a lack of lending activity in the debt markets have contributed to considerable weakness in the commercial real estate markets.

There are many factors in addition to changes to our real estate values from our estimates that may affect the amount of liquidating distributions available for distribution to our stockholders, including, among other factors: (i) changes in market demand that affect the timing of the disposition of our properties during the liquidation process, (ii) the amount of taxes, transaction fees and expenses relating to the Plan of Liquidation, and (iii) amounts needed to pay or provide for our liabilities and expenses, including unanticipated or contingent liabilities that could arise. No assurance can be given as to the amount of liquidating distributions you will ultimately receive. If we have underestimated our existing obligations and liabilities or if unanticipated or contingent liabilities arise, the amount ultimately distributed to our stockholders could be less than that set forth above. All of these factors could adversely impact the amount of liquidating distributions we pay to our stockholders. See “Risk Factors” and “Proposal 1: The Plan of Liquidation Proposal – Background of the Plan of Liquidation.”

Q. Including the estimated liquidating distributions per share, if the Plan of Liquidation Proposal is approved, what will be the cumulative per share amount of distributions paid to the Company’s stockholders?

A. Assuming the Plan of Liquidation Proposal is approved, the cumulative amount of distributions a stockholder receives from us will vary depending on the date on which the stockholder purchased their shares and will generally be unique to each stockholder. We note that from inception, the Company has paid distributions, including a special distribution in November 2015 in cash and common stock, of $29,106,639. Based solely on the 10,957,289 fully diluted shares currently outstanding and the total amount of distributions paid by the Company since inception, distributions per share since inception would equal $2.66. As the Company has issued and redeemed shares over the course of its life cycle this distributions per share since inception number is not representative of distributions received by any one stockholder. In addition, it does not take into account amounts invested and paid for the redemption of common stock. Stockholders who purchased shares earlier in the offering would have received more than this amount and stockholders who purchased shares later in the offering would have received less than this amount. However, based solely on this estimate of distributions per share since inception, a stockholder may receive total cumulative distributions (including the estimated range of liquidating distributions per share), that range between $3.77 and $4.08 per share. Stockholders should consult their individual account statements for information regarding distributions received from the Company to date. Further, see “If the Plan of Liquidation Proposal is approved, what do you estimated that the Company’s stockholders will receive?” above for a discussion of the factors that could cause our range of estimated liquidating distributions per share to vary from our estimate.

Q. When will I receive my liquidating distributions?

A. If the Plan of Liquidation is approved by our stockholders, we may pay multiple, or a single, liquidating distribution payment(s) to our stockholders during the liquidation process. The final liquidating distribution will be paid after we sell all of our properties, pay all of our known liabilities and provide for unknown liabilities. We expect to complete these activities within 24 months after stockholder approval of the Plan of Liquidation. However, the completion of these activities may be delayed due to the continuing impact of the ongoing challenges affecting the U.S. commercial real estate industry, including the continued economic slowdown, rising interest rates and significant inflation (or the perception that any of these events may continue), and a lack of lending activity in the debt markets which may impact the ability of buyers for our properties to obtain favorable financing. If we have not sold all of our properties and paid all of our liabilities within 24 months after stockholder approval of the Plan of Liquidation, or if the board of directors otherwise determine that it is advantageous to do so, we may transfer our remaining assets and liabilities to a liquidating trust. We would then distribute beneficial interests in the liquidating trust to our stockholders. If we establish a reserve fund, we may pay a final distribution from any funds remaining in the reserve fund after we determine that all of our liabilities have been paid.

The actual amounts and timing of the liquidating distributions will be determined by the board of directors or, if a liquidating trust is formed, by the trustees of the liquidating trust, in their discretion. If you transfer your shares during the liquidation process, the right to receive liquidating distributions will transfer with those shares.

Q. What is a liquidating trust?

A. A liquidating trust is a trust organized for the primary purpose of liquidating and distributing the assets transferred to it. If we form a liquidating trust, we will transfer to our stockholders beneficial interests in the liquidating trust. This transfer of beneficial interests will constitute a taxable distribution to you in redemption of your ownership of our common stock. Beneficial interests in the liquidating trust will generally not be transferable by you.

Q. What will happen to my shares of stock?

A. If our stockholders approve the Plan of Liquidation Proposal, after we have sold all of our assets, satisfied our liabilities, paid our final liquidating distribution to our stockholders and filed the Articles of Dissolution with the SDAT, all shares of our common stock owned by you will be cancelled.

Q. Do your directors and officers, SRT Advisor or its affiliates have any interests in the liquidation that differ from my own?

A. Yes, some of our directors and officers and SRT Advisor and its affiliates may have interests in the liquidation that are different from your interests as a stockholder, including the following:

•SRT Advisor earns asset management fees from us and receives reimbursement of certain of its operating costs. SRT Advisor will continue to earn such fees and receive reimbursements as long as we continue to own any properties, and SRT Advisor will receive reimbursements for expenses until our liquidation and dissolution are complete. Assuming upon renewal of the Advisory Agreement, the asset management fee remains capped at $250,000 in the aggregate for a twelve-month period commencing August 2023, we project that we may pay SRT Advisor an aggregate of approximately $396,000 for asset management fees and reimbursement of certain of its operating expenses in 2023 and 2024 during the liquidation process, although this estimate may vary significantly based on the timing of property sales.

•SRT Advisor may be entitled to disposition fees in connection with the sale of our assets. If the independent directors determine that SRT Advisor or any of its affiliates provides a substantial amount of services in connection with a sale, SRT Advisor or such affiliate will receive a fee at the closing of the sale equal up to 50% of a competitive real estate commission, but not to exceed 3% of the contract sales price. These disposition fees are estimated to be between approximately $1,006,000 and $1,117,000, depending upon and correlated to the price we receive for the sale of our assets.

Consequently, some of our directors and officers and SRT Advisor, in some instances, may be more motivated to support the Plan of Liquidation than might otherwise be the case if they did not expect to receive those payments. Additionally, because of the above potential conflicts of interest, some of our directors and officers and SRT Advisor may be motivated to make decisions or take actions based on factors other than the best interest of our stockholders throughout the liquidation process. The board of directors was aware of these interests and considered them in making their recommendations. For further information regarding interests that differ from your interests please see “Proposal 1. The Plan of Liquidation Proposal Interests in the Plan of Liquidation that Differ from Your Interests.”

Q. Are there any risks related to the Plan of Liquidation?

A. Yes. You should carefully review the section of this proxy statement entitled “Risk Factors.”

Q. What are the United States federal income tax consequences of the Plan of Liquidation?

A. Subject to the limitations, assumptions, and qualifications described in this proxy statement and the approval by our stockholders of the Plan of Liquidation, the intended liquidation and dissolution of the Company pursuant to the Plan of Liquidation will constitute a taxable distribution to you in redemption of your ownership of our common stock, with the following material federal income tax consequences to our stockholders.

In general, if the Plan of Liquidation is approved and we are liquidated, you will realize, for U.S. federal income tax purposes, gain or loss equal to the difference between the cash distributed to you by the Company and your adjusted tax basis in our common stock. Note that any loss inherent in your common stock would not be recognizable until the final liquidating distribution is made, which would likely be during the 2025 taxable year. If we distribute beneficial interests in a liquidating trust (as defined in the section entitled “Material United States Federal Income Tax Consequences” in this proxy statement) to you, you would be required to recognize any gain in the taxable year of the distribution of the liquidating trust beneficial interests (to the extent that you have not recognized such gain in prior taxable years), although you may not receive the cash necessary to pay the tax on such gain. If you receive cash from the liquidating trust, you may receive such cash after the due date for filing your tax return and paying the tax on such gain. Distributions of beneficial interests in the liquidating trust will also constitute a final liquidating distribution that should allow the recognition of any loss. A summary of the possible tax consequences to you is included in “Material United States Federal Income Tax Consequences” in this proxy statement.

YOU ARE URGED TO CONSULT YOUR OWN TAX ADVISOR AS TO THE SPECIFIC TAX CONSEQUENCES TO YOU OF THE TRANSACTIONS DESCRIBED IN THIS PROXY STATEMENT, INCLUDING THE APPLICABLE FEDERAL, STATE, LOCAL, AND FOREIGN TAX CONSEQUENCES OF SUCH TRANSACTIONS.

Q. Why is the Company seeking a stockholder vote on the Adjournment Proposal?

A. Adjourning the annual meeting to a later date will give us additional time to solicit proxies to vote in favor of any proposal that has not received sufficient votes to be approved at the annual meeting. Consequently, we are seeking your approval of the Adjournment Proposal to permit us (i) to proceed with the voting on and approval of only the proposals that have received sufficient votes to be approved at the annual meeting, and (ii) subsequently, to adjourn the annual meeting to solicit additional proxies to vote in favor of any proposal that has not received sufficient votes to be approved at the annual meeting.

RISK FACTORS

The following risk factors, together with the other information in this proxy statement and in the “Risk Factors” sections included in the documents incorporated by reference in this proxy statement (see “Where You Can Find More Information”), should be carefully considered by each of our stockholders before deciding whether to vote to approve the Plan of Liquidation Proposal as described in this proxy statement. In addition, our stockholders should keep in mind that the risks described below are not the only risks that are relevant to a voting decision. The risks described below are the risks that we currently believe are the material risks of which our stockholders should be aware. However, additional risks that are not presently known to us, or that we currently believe are not material, may also prove to be important.

RISKS THAT MAY DELAY OR REDUCE OUR LIQUIDATING DISTRIBUTIONS

We currently estimate that, if the Plan of Liquidation Proposal is approved by our stockholders and we are able to implement the plan successfully, our liquidating distributions per share and, therefore, the amount of cash that you would receive for each share of our common stock that you then hold, would range between approximately $1.11 and $1.42 per share. We anticipate paying our liquidating distributions from the net proceeds from liquidation within 24 months after stockholder approval of the Plan of Liquidation. However, our expectations about the amount of liquidating distributions that we will pay and when we will pay them are based on certain estimates and assumptions, one or more of which may prove to be incorrect. As a result, the actual amount of liquidating distributions we pay to you may be more or less than we estimate in this proxy statement and the liquidating distributions may be paid later than we predict. In addition to the risks that we generally face in our business, factors that could cause actual liquidating distribution payments to be lower or paid later than we expect include, among others, the risks set forth below.

If any of the parties to our future sale agreements default thereunder, or if these sales do not otherwise close, our liquidating distributions may be delayed or reduced.

If you approve the Plan of Liquidation, we will seek to enter into binding sale agreements for each of our properties. The consummation of the potential sales for which we will enter into sale agreements in the future will be subject to satisfaction of closing conditions. If any of the transactions contemplated by our future sale agreements do not close because of a buyer default, failure of a closing condition or for any other reason, including the COVID-19 pandemic or other pandemics or outbreaks, political or economic instability or social unrest, the rising interest rate environment that is impacting the ability of buyers to obtain favorable financing, we will need to locate a new buyer for the properties, which we may be unable to do promptly or at prices or on terms that are as favorable as the original sale agreement. We will also incur additional costs involved in locating a new buyer and negotiating a new sale agreement for these properties. These additional costs are not included in our projections. In the event that we incur these additional costs, our liquidating distributions paid to you would be delayed or reduced.

If we are unable to find buyers for some or all of our properties within our expected timeframe or at our expected sales prices, our liquidating distributions may be delayed or reduced.

We have targeted disposition plans and timeframe estimates for each of the remaining assets of the Company. We will market our properties for sale over the coming months if our stockholders approve the Plan of Liquidation Proposal. There can be no assurance that any of our properties will sell within our expected timeframe or for their projected sales prices.

In calculating the range of estimated liquidating distributions per share, we assumed that we will be able to find buyers for all of our properties at amounts based on our estimated range of market values for each property. However, we may have overestimated the sales prices that we will ultimately be able to obtain for these assets. For example, in order to find buyers in a timely manner, we may be required to lower our asking price below the low end of our current estimate of the property’s market value. If we are not able to find buyers for these assets in a timely manner or if we have overestimated the sales prices we will receive, our liquidating distributions paid to you would be delayed or reduced. Furthermore, the range of estimated liquidating distributions per share is based upon our estimates and assumptions as of May 12,2023, but real estate market values are constantly changing and fluctuate with changes in interest rates, supply and demand dynamics, occupancy rates, rental rates, the availability of suitable buyers and financing, the perceived quality and dependability of cash flows from properties and a number of other factors, both local and national.

In particular, global markets continue to experience significant volatility, driven by concerns over persistent inflation, rising interest rates, slowing economic growth and geopolitical uncertainty. These events as well as COVID-19 and other possible pandemics and outbreaks, political or economic instability, social unrest or other disruptions or events outside of our control may adversely affect our ability to locate buyers for our remaining properties, may delay the completion of the sales of such properties or adversely affect the price at which such properties may be sold. In addition, higher than anticipated transactional fees and expenses, environmental liabilities of which we are unaware or other unknown liabilities, if any, may adversely impact the net liquidation proceeds from those assets.

No assurance can be given as to the amount or timing of liquidating distributions you will ultimately receive. For more information on the calculation of our range of estimated liquidating distributions per share, see “Proposal 1. The Plan of Liquidation Proposal – Calculation of the Range of Estimated Liquidating distributions per share.”

Elevated market and economic volatility due to adverse economic and geopolitical conditions (such as the war in Ukraine), health crisis (such as the continuing impact of the COVID-19 pandemic), concerns over persistent inflation, rising interest rates and slowing economic growth, could have material and adverse effects on our ability to complete the Plan of Liquidation within our expected timeframe or upon the terms we expect, which could reduce or delay our liquidating distributions.

Our ability to implement the Plan of Liquidation successfully and pay liquidating distributions to our stockholders may be adversely affected by market and economic volatility experienced by the U.S. and global economies, the U.S. retail market as a whole and/or the local economies in the markets in which our properties are located. Such adverse economic and geopolitical conditions may be due to, among other issues, increased labor market challenges impacting the recruitment and retention of employees, rising inflation and interest rates, volatility in the public equity and debt markets, and international economic and other conditions, including pandemics (such as the continuing impact of the COVID-19 pandemic), geopolitical instability (such as the war in Ukraine), sanctions and other conditions beyond our control. These current conditions, or similar conditions existing in the future, may adversely affect our financial condition and ability to complete the Plan of Liquidation within our expected timeframe or upon the terms we expect as a result of one or more of the following, among other potential consequences:

•revenues from our properties could decrease due to fewer tenants and/or lower rental rates, making it more difficult for us to meet our debt service obligations on debt financing or reducing liquidating distributions available for our stockholders.

•the financial condition of our tenants may be adversely affected, which may result in tenant defaults under leases due to bankruptcy, lack of liquidity, lack of funding, operational failures or for other reasons;

•our ability to borrow on terms and conditions that we find acceptable, or at all, may be limited, which could reduce our ability to refinance existing debt and increase our future interest expense;

•the ability of potential purchasers of our assets to access the debt markets on favorable terms and conditions may be limited due to the current rising interest rate environment;

•reduced values of our properties and revenues from our properties may (i) limit our ability to dispose of assets at attractive prices, (ii) limit our ability to obtain debt financing secured by our properties, and (iii) reduce the availability of unsecured loans;

•the value and liquidity of our short-term investments and cash deposits could be reduced as a result of a deterioration of the financial condition of the institutions that hold our cash deposits or the institutions or assets in which we have made short-term investments, a dislocation of the markets for our short-term investments, increased volatility in market rates for such investments or other factors; and

•to the extent we enter into derivative financial instruments, one or more counterparties to our derivative financial instruments could default on their obligations to us, or could fail, increasing the risk that we may not realize the benefits of these instruments.

Specifically, in order to successfully complete the Plan of Liquidation, we must identify and complete one or more transactions with third parties for the sale of our remaining properties. The success, timing and terms of such transactions may be adversely impacted by the continued impacts of the COVID-19 pandemic on the market for retail real estate in the United States. Even if we are able to identify potential buyers, such buyers may have difficulty accessing debt and equity capital on attractive terms, or at all, due to rising interest rates, disruptions in the global financial markets or deteriorations in credit and financing conditions, which may affect their access to capital necessary to consummate the acquisition of our properties. If financing is unavailable to potential buyers of our properties, or if potential buyers are unwilling to engage in various transactions due to the uncertainty in the market, our ability to complete such dispositions within our expected timeframe or on the expected terms would be significantly impaired. In addition, reduced economic activity and general economic decline or recession may impact our tenants’ businesses, financial condition and liquidity and may cause one or more of our tenants to be unable to make rent payments to us timely, or at all. The continuing impact of the COVID-19 pandemic, elevated market and economic volatility due to adverse economic and geopolitical conditions and the impact on potential buyers, our tenants and general economic conditions may adversely affect our ability to close dispositions of our remaining properties and complete our Plan of Liquidation in a timely manner, upon satisfactory terms, or at all, which could cause the liquidating distributions paid to you to be delayed or reduced.

If we experience significant lease terminations and/or tenant defaults during the liquidation process or if our cash flow during the liquidation process is otherwise less than we expect, our liquidating distributions may be delayed or reduced.

In calculating our range of estimated liquidating distributions per share, we assumed that we would not experience significant lease terminations not currently known to us and that we would not experience any significant unknown tenant defaults during the liquidation process that were not subsequently cured. In addition, we assumed that our properties would continue to operate consistent with past practice, including that our tenants would continue to pay rent and operate their business in the ordinary course. Any currently known lease expirations and non-renewals of tenant leases or other events that would impact our collection of rents were considered in calculating our range of estimated liquidating distributions per share. Significant unknown lease terminations and/or tenant defaults or other reductions to our rental income during the liquidation process, would adversely affect the resale value of the properties, which would reduce our range of estimated liquidating distributions per share. To the extent that we receive less rental income than we expect during the liquidation process, our liquidating distributions will be reduced. We may also decide in the event of a tenant default to restructure the lease, which could require us to substantially reduce the rent payable to us under the lease, or make other modifications that are unfavorable to us.

If our liquidation costs or unpaid liabilities are greater than we expect, our liquidating distributions may be delayed or reduced.

Before paying the final liquidating distribution, we will need to pay or arrange for the payment of all of our transaction costs in the liquidation, all other costs and all valid claims of our creditors. The board of directors may also decide to acquire one or more insurance policies covering unknown or contingent claims against us, for which we would pay a premium that has not yet been determined. The board of directors may also decide to establish a reserve fund to pay these contingent claims. The amounts of the various transaction costs in the liquidation are not yet final, so we have used estimates of these costs in calculating the amounts of our range of estimated liquidating distributions per share. To the extent that we have underestimated these costs in calculating our projections, our actual liquidating distributions per share may be lower than the low end of our range of estimated liquidating distributions per share. In addition, if the claims of our creditors are greater than we have anticipated or we decide to acquire one or more insurance policies covering unknown or contingent claims against us, our liquidating distributions may be delayed or reduced. Further, if we establish a reserve fund, payment of liquidating distributions to you may be delayed or reduced.